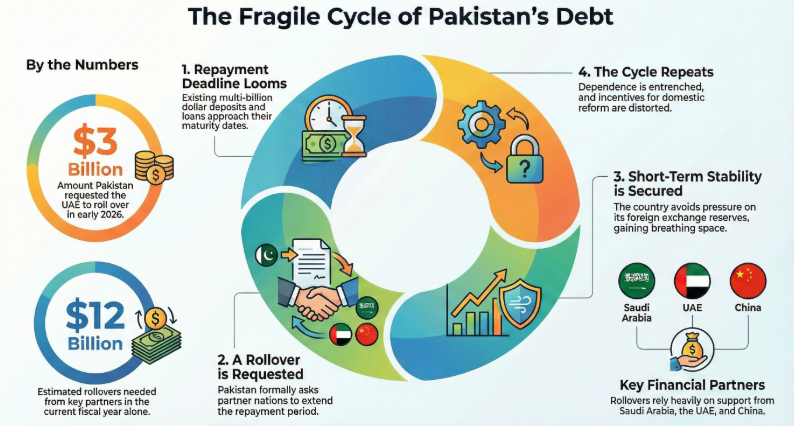

Pakistan’s recent request to the United Arab Emirates (UAE) to roll over 3 billion dollars of deposits once again highlights how the country’s macroeconomic stability hinges on external bailouts rather than durable structural reforms.This pattern of repeated rollovers and emergency funding from friendly states and multilateral institutions has provided short-term breathing space but has also entrenched a fragile economic model that discourages domestic reform, distorts incentives, and perpetuates dependence.

In early January 2026, Pakistan formally approached the UAE leadership to roll over 3 billion dollars currently parked with the State Bank of Pakistan (SBP) in three separate 1 billion dollar tranches, originally deposited in 2021 to shore up Pakistan’s balance of payments. Two of these tranches are due in the second and third weeks of January 2026, with the remaining 1 billion dollars expected to mature later in the year, prompting the government to seek extension of all three before maturity to avoid renewed pressure on its foreign exchange reserves.

Official sources have indicated that Pakistan expects the rollover process to be completed on time and has also assured the International Monetary Fund (IMF) that the UAE will maintain these deposits in line with commitments made under the ongoing IMF program. This request is systematic in which Pakistan leans heavily on bilateral partners, notably Saudi Arabia, the UAE and China to roll over central bank deposits and commercial loans whenever repayment deadlines approach. For the current fiscal year, government sources estimate that Pakistan will rely on rollovers of around 12 billion dollars from these three partners alone, underscoring how the country’s external account management has become structurally tied to friendly capital rather than domestic export capacity or productivity-led growth.

The SBP governor recently highlighted that in fiscal year 2025–26 total external repayments amount to about 25.8 billion dollars, of which approximately 9.3 billion dollars are expected to be rolled over, illustrating how rollovers are now embedded as a routine pillar of debt management rather than an exceptional crisis tool.

Multilateral financing has similar narrative. In September 2024, the IMF Executive Board approved a new 7 billion dollar, 37‑month Extended Fund Facility (EFF) for Pakistan, with disbursement contingent on “sound policies and reforms” but also explicitly underpinned by substantial financing assurances and rollovers from China, Saudi Arabia, and the UAE. IMF officials have acknowledged that Pakistan has already been through 22 previous IMF programs since 1958, a frequency that itself is symptomatic of recurring external sector crises and the failure of past reform efforts to break the cycle of dependence. Under the new program, Pakistan secured immediate disbursement of 1 billion dollars and additional commitments, yet the conditionality again focuses on stabilisation rather than a fundamental restructuring of the economic model.

Pakistan’s external accounts data underline how fragile this model remains despite episodic improvements. The IMF’s first review of the new EFF notes that gross international reserves stood at 10.7 billion dollars at end‑March 2025, down from a peak of 12 billion dollars in November 2024, even after meeting program targets, reflecting continuous debt servicing and the need for FX market interventions. Earlier documents highlight that reserve accumulation in FY24–25 has been heavily supported by remittances and resilient exports, but these positive flows have had to offset high external debt repayments and the country’s elevated import needs, particularly for energy.

Even the more positive assessments stress that the apparent improvement in reserves rests on a fragile foundation. By mid‑2025, SBP reserves reportedly touched about 14.5 billion dollars, giving Pakistan around 2.5 months of import cover and exceeding certain IMF benchmarks, but this followed a period when reserves had dropped below 4 billion dollars in 2022–23, barely enough for three weeks of imports. The restoration of reserves has been aided by non‑debt inflows such as better exports, higher IT services receipts, and record remittances, yet the high‑frequency reliance on bilateral deposits and IMF disbursements shows that Pakistan has not secured a structurally self‑sustaining external position. Each rollover pushes the risk of a crisis forward but leaves the underlying vulnerabilities intact, creating a chronic dependence on the goodwill of a narrow set of external partners.

Pakistan’s own official documents acknowledge this structural vulnerability. The Pakistan Economic Survey’s chapter on trade and payments notes that the country’s economic history has been marked by cycles of external borrowing, fiscal imbalances, and exchange‑rate volatility, leading to recurrent IMF programs as a stabilising mechanism rather than as a one‑time adjustment tool. The same analysis stresses that Pakistan’s import dependence is particularly acute, with China, Saudi Arabia, the UAE and Indonesia together accounting for nearly half of the country’s imports, which magnifies exposure to commodity price shocks and supply disruptions.

As a result, external shocks quickly translate into BOP stress, forcing Pakistan back to the IMF and friendly capitals for short‑term financing, rollovers and deposits. This external dependence has profound structural consequences. Continuous rollovers and crisis‑driven bailouts blunt domestic reform incentives by creating a perception among policymakers that friendly states and multilateral lenders will not allow Pakistan to default, thereby weakening the urgency for tough tax, energy and governance reforms. Instead of broadening the tax base, cutting quasi‑fiscal losses, and boosting productivity, successive governments have opted for politically easier strategies like import compression, ad hoc subsidies, and repeated renegotiation of external debt terms.

IMF reviews explicitly call for stronger tax collection from under‑taxed sectors such as retailers and for better targeted public spending, but Pakistan’s track record suggests that most adjustment is borne by compliant taxpayers and consumers through inflation, energy tariff hikes, and currency depreciation rather than by structural reordering of the political economy. At the same time, heavy reliance on deposits and loans from a narrow group of partners constrains Pakistan’s strategic and economic autonomy. The requirement to maintain “friendly” political positions to secure rollovers from Riyadh, Abu Dhabi, and Beijing introduces an external dimension to domestic economic policy choices and foreign policy decision-making.

Pakistan’s request for a 3 billion dollar rollover from the UAE is emblematic of a deeper structural malaise rather than just a routine financing operation. As long as external deposits, IMF bailouts and bilateral rollovers remain the primary instruments of macroeconomic management, the country will continue to oscillate between short-lived episodes of stability and recurring crises, with each new program layered on top of unresolved structural distortions.

Lastly, the success of Pakistan’s reliance on the same set of patrons is itself questionable. China has understood Pakistan’s readiness to compromise iron-brotherhood for US’s overtures and framing of bilateral engagement to counter China’s influence in the region. Recently, in view of bilateral defence pact, Saudi Arabia has warned Pakistan on its approach towards Saudi-UAE conflict in Yemen. UAE too have noted Pakistan’s plan to sell waepons worth US $ 1.5 billion to Sudan which is bound to be used against UAE supported Rapid Support Forces. All these are set to make the economic rollover process much more vulnerable for Pakistan.